Technology has been changing the shape of everything we do. Machines are not just helping us in the operational parts of investing but they are also assisting us with their investment decisions majorly driven by Artificial Intelligence and Machine Learning techniques.

In many ways, we’re not just competing with other smart investors but with investors and their sophisticated batteries of machines. Algorithmic trading is a mysterious black box to most people in the world even today. There is often little understanding even amongst finance professionals regarding the inner workings of “algos”.

Who does not know this person?

No one. Everyone knows he is the legendary investor ‘THE WARREN BUFFET’

Now, who knows about him?

Very few…right?

This person has had a track record, which arguably is far, far better than what Buffett has achieved. But most people don’t know about him. It’s recently that I got aware of him and his organization from a book written by Wall Street journalist Gregory Zuckerman – “The Man Who Solved The Market”. Although it was a fun read, the book still does not reveal much about how the Algo-strategies are built.

Let’s deep dive into this topic then…

So, who is the greatest investor in history?

The name of Warren Buffet usually pops up in an average investor’s mind but it isn’t the Oracle of Omaha who has the top spot instead,

The top dog distinction in the world’s top investors belongs to a former mathematics professor most investors never heard of:

He is Jim Simons!

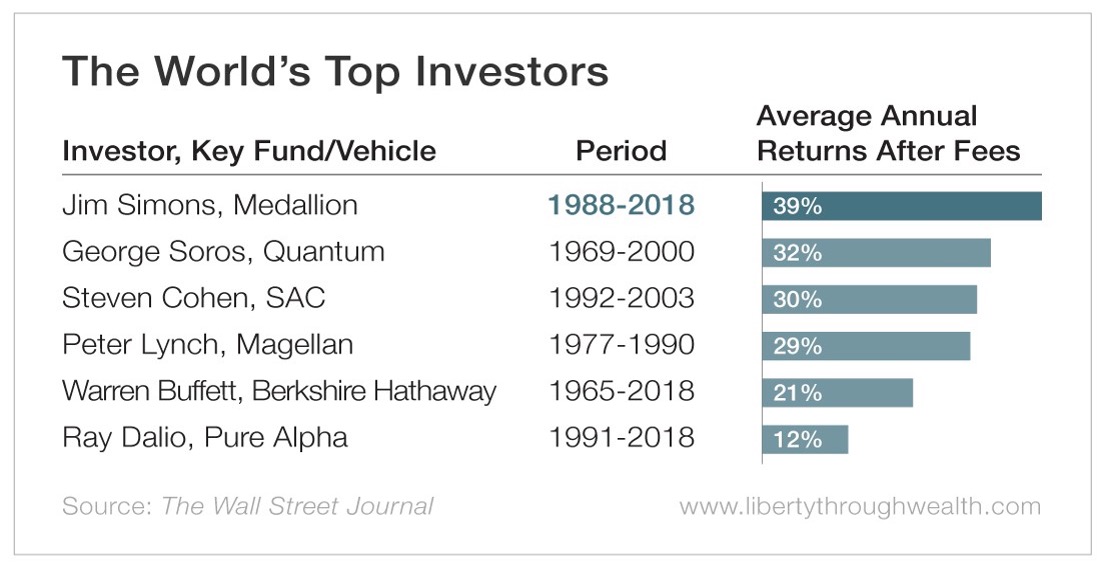

Jim Simons is the Founder of Renaissance Technologies that manages a multibillion-dollar Medallion Fund. He is the person in the above picture who is not easily recognized by many investors around the world. Renaissance’s flagship Medallion fund has generated a whopping average annual return of 66% before fees since 1988 that narrows down to 39% after its hefty fees – 5% of all assets managed and 44% of all gains.

Buffett doesn’t have this kind of record right?

Seems impressive, right? But what is the first reaction or question that comes to mind?

Is he taking too much risk? Is this another Ponzi scheme? Is he a fraud?

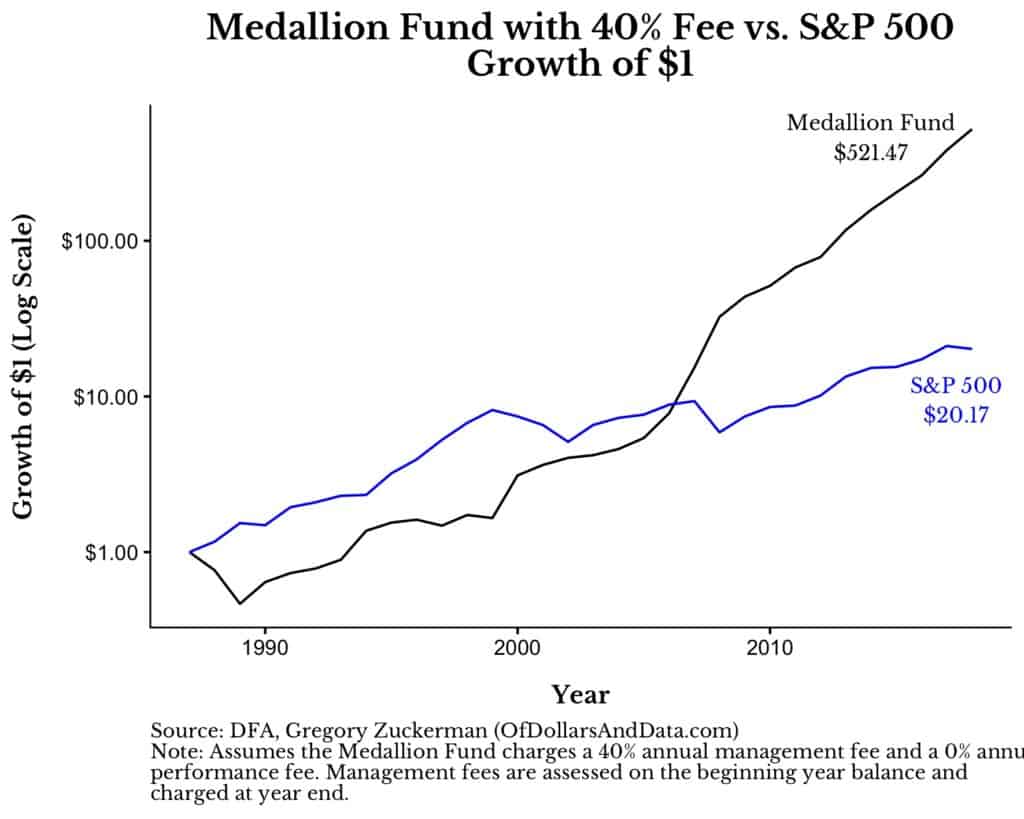

Well, if something sounds too good to be true, usually it is. But let’s see the below graph which compares the returns of Medallion Fund and the S&P 500 stock index to get more clarity…

The above graph compares and puts the performance of the Medallion fund and S&P 500 in perspective. A $1 investment in the Renaissance’s Medallion Fund from 1988-2018 would have returned over $20,000 (not considering fees) while the same investment in the S&P 500 stock market index would have returned $20 over the same period. Even a $1 investment in Warren Buffet’s Berkshire Hathaway would have “only” grown to $100 during the same period of time.

This means that the Medallion Fund outperformed one of the best asset classes of the last few decades by 1,000x and one of the best investors of all time by 200x!

Apart from the absolute numbers, the fact that even in catastrophic years such as 2008 Jim Simons didn’t lose money is again something which would arouse curiosity!

Medallion’s Secret Sauce

Renaissance technologies do not rely on the fundamentals of the company instead, they focus their efforts on developing quantitative investment strategies by using high computing power. As a matter of fact, the company does not employ any CFAs or MBAs.

In fact, it’s almost like a disqualification!

People who are recruited in the firm are math & stats professionals, computer programmers, physicists, or people who have been working in the early stage of machine learning, natural language processing.

The Medallion fund finds inefficiencies in the market by sifting through the market noise to find repeating patterns that are statistically different. Quantitative strategies are executed to trade these patterns in the short term across various asset classes like stocks, bonds, futures, commodities, and currencies. Renaissance leverages its bets and magnifies its returns through these robust, short-term predictions.

Do you want to learn more about Jim Simon’s strategies or Quants in general?

Let’s clear a few MYTHS about Algo/Quants…

- It has to be fully automated, requires high-performance computers and deep domain programming expertise

- It carries very high/very low risk

- Algo/Quant based trading is pure arbitrage

- It can’t do as well as value investing

Well, people talk about transaction costs, high-frequency trading, efficient market hypothesis, and lots of other stuff… But how do quants/algos help the new-age investors?

Why does it work?

- Objective systems ignore human biases and are less prone to behavioral mistakes

- The ability to back-test strategies

- Algo-strategies are often scalable and easily replicable across markets and asset classes

- Advantages of speed efficiency and accuracy in executing strategies

Let’s talk about the inputs required for algorithmic trading strategies or data required to make a quant-based investment decision…

So, there are six broad categories of data that can power any Algo-trading strategies/investment decisions:

- Daily Market Data (The typical OHLC and Volume data)

- Fundamental Data (Data related to corporate actions and financial statements)

- Macroeconomic Data (Interest rates, employment, inflation, GDP to market cap, etc.)

- News (How subjective news can take objective decisions?)

- High-Frequency Data (Market order flow data)

- Alternative Data (Emerging data sources like- satellite imagery, weather data, airline movement data, social media sentiment, etc.)

Earlier in this article, we talked about how decisions need to be objective; but then how to process the news? Here, a variety of things are being done – some news sources such as Reuters and Bloomberg have machine-readable feeds for some specific kinds of news especially interest rate announcements by RBI, other macroeconomic data, etc.

In this way, when RBI announces a change in the repo rate, a program can react to the number and make a trade instantly. However, by using machine learning it is also possible to process natural language news to identify events like acquisitions, product launches, workers’ strikes, and even a general sentiment about the company. These can then be turned into triggers to buy and sell securities.

Going forward let’s see how high-frequency data helps in decision making

High-frequency data is the market order flow data, and depending on the exchange you can get information about every single order placed and canceled in the market. These are extremely rich data sets and an ideal playground for statisticians and big data geeks.

We’re talking about millions of orders a day which requires high computing power to process the data meaningfully. Some very low profile but extremely successful firms use this kind of data to make all or most of their money which includes firms like Tower Research Capital, Tradebot, Virtu Financial, and Hudson River Trading.

Finance is not a pure science rather it is social science!

It is exactly the sort of environment where Deep Learning can be a perfect fit. Quants are going through a fundamental transition right now where instead of helping traders to do the math they are majorly focused on data-science-driven decisions.

Subscribe to our Newsletter to get exciting content delivered to your Mailbox!

{kind=link}